Electric heating boiler classification and characteristics

This article was first published on WeChat public number: New Energy Network Energy. The content of the article belongs to the author's personal opinion and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk.

|

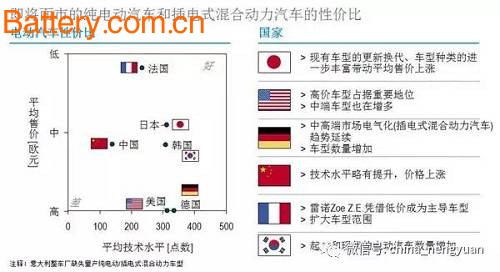

In terms of “technical†indicators, Germany has surpassed Japan (second) and South Korea (third), ranking first with France. The reason for this is that German automakers have significantly increased the production of pure electric and plug-in hybrid vehicles, and on the other hand, because Germany can provide users with longer prices while keeping prices unchanged. The cruising range. French automakers are still focusing on low-cost, small-scale pure electric vehicles . Although the product range is not as good as that of German manufacturers, the price/performance ratio is still high. In contrast, Korean OEMs have a limited range of products, mainly in plug-in hybrid vehicles, and the time-to-market for such vehicles may be significantly delayed. Chinese automakers have relatively few moves, and although many new models are planned to be launched in the next few years, they are still mainly targeted at areas with low technology content. American automakers are gradually shifting their products from high-margin high-end cars to the more popular mid-range car market. The main goal of Japanese automakers is to upgrade existing products, and only some automakers plan to enrich their product portfolio in the medium term. The price of lithium batteries has generally accelerated. The cars will be applied quickly after 2018. This will enable OEMs to increase the production of long-distance battery life. The medium-term product portfolio will undergo more profound changes (see Figure 1). ).

|

In terms of the scale of national electric vehicle R&D projects, as some R&D projects are nearing completion, there will be some minor changes in some countries such as China, but the relative status of the world's leading seven auto powers has not changed fundamentally, and countries will still Continue to carry out investment projects aimed at optimizing the technical system. In addition to funding research and development projects, countries have also promoted market prosperity and expansion of infrastructure through subsidies, such as the recent purchase of car discounts in Germany and the construction of charging stations (see Figure 2).

|

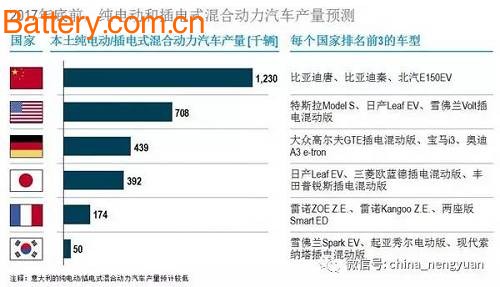

As far as the “industry†indicator is concerned, China has established a leading position because the country's market continues to grow rapidly and more than 90% of lithium batteries are produced locally. The reason for this high localization rate is partly because the government subsidies are limited to companies that create value for the local market, and foreign battery manufacturers are often unable to build factories in China due to qualification restrictions. Compared with China, Japan is at a disadvantage in both electric vehicle production and global battery production share, ranking third in the world. The United States climbed to second place. At the same time, regional market differentiation in the United States and Europe is increasingly apparent. German automakers dominate the European market, and US automakers dominate the North American market, but neither has penetrated the Asian market in large numbers (see Figure 3).

|

In the field of battery manufacturing, China's advantages are increasingly obvious.

From the perspective of global battery production share, Chinese battery manufacturers are already in a leading position. But it is worth noting that Korean battery manufacturers are gradually gaining market share by producing batteries in China. In addition, Korean and Japanese battery manufacturers have announced the deployment of localization projects in the United States, and in the medium term, they are expected to deploy similar projects in the European market. With the expansion of the long-distance battery life of pure electric vehicles, the demand for batteries will continue to grow; at the same time, battery prices will fall sharply. Under the combined effect of these two major trends, the market scale can only achieve a modest amount of net growth. The need for greater battery capacity, coupled with a constant automotive market size, will drive a significant increase in battery maker investment (see Figure 4).

|

From the perspective of “marketâ€, China’s demand has increased significantly, and it is now second only to France. Although the absolute number of electric vehicles in France is much lower than that of China, it has a higher market share. The United States ranks third. Compared with the previous quarter, China's sales have more than doubled; both Germany and France have increased by about 50%; Japan has also performed well, achieving double-digit growth. In comparison, the growth rate of the United States and Italy has slowed significantly, both of which are within 10%. In the United States, plug-in hybrid vehicles are gradually replacing all-hybrid vehicles, bringing new demands and preventing the United States from slowing down even more. South Korea has seen a single-digit decline. As mentioned above, in the medium term, the proportion of pure electric vehicles with a range of more than 300 kilometers will increase. However, in 2016, pure electric and plug-in hybrid vehicles had a market share of less than 2% in China and France. Therefore, in order to achieve the emission targets introduced after 2021, this market share in Europe still needs to increase significantly (see Figure 5).

|

The report also pointed out that China has significantly revised its vehicle emission standards to promote the sales of various types of electric vehicles.

In 2014-2015, sales of pure electric and plug-in hybrid vehicles in China more than tripled to 330,000. Therefore, in terms of sales volume, China is not only the world's largest passenger car market, but also the largest plug-in hybrid power and pure electric vehicle market. However, like other countries, China's pure electric and plug-in hybrid vehicles accounted for less than 1% of total vehicle sales in 2015. China still needs various measures to achieve the goals set in the 13th Five-Year Plan. To ensure that the number of electric vehicles will reach 5 million by 2020.

The Chinese government believes that electric vehicles are a huge opportunity to enhance global competitiveness and reduce China's dependence on imported oil. In this regard, the Chinese government has planned a comprehensive policy framework to enable OEMs to achieve the goal of 7% of sales of pure electric and plug-in hybrid vehicles in 2020 and 19% of sales in 2025; However, its current market share is less than 2% on average.

The mechanism currently under consideration is to combine the average fuel consumption of enterprises (CAFC) with the points of new energy vehicles. The new energy vehicle points can be used to offset the CAFC negative points, and the new energy vehicle points can also be traded. Industry experts believe that the transaction price of a new energy vehicle point will be between 7,500-10,000 yuan. This provision is still in the discussion stage and is expected to be implemented as early as 2018.

|

Funke Gasket Heat Exchangers,Funke Phe Gasket,Funke Heat Exchangers Gaskets,Phe Gasket For Funke

Dongguan Runfengda F&M Co., Ltd , https://www.nbrfdphe.com